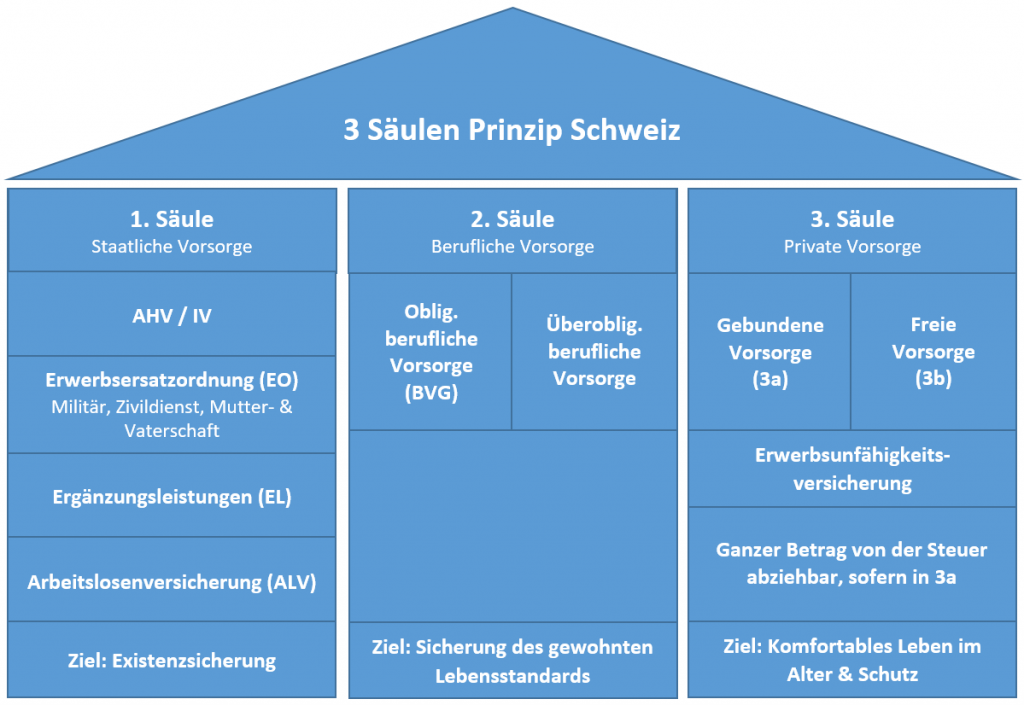

Fundamentals of old-age and survivors’ insurance (AHV)

Why the 1st pillar?

The purpose of the 1st pillar is to minimise the economic consequences of common risk factors, namely:

- Economic consequences of old age (AHV)

- Economic consequences of death (AHV)

- Economic consequences of disability (IV)

The pension from the AHV is very small and limited to a maximum of CHF 2,390 per month (as of 2021). It only serves to secure your livelihood.

In order to receive this CHF 2,390 in the 1st pillar, you must have an average salary of at least CHF 86,040 during your working career according to scale 44, and you must not have missed any of the 44 contribution years (43 years for women).

Combined with the 2nd pillar, the pension amounts to approx. 60% of the previous earned income.

Since the pension, especially for married couples, is a maximum of CHF 3,585, there is an enormous income gap.

Who is compulsorily insured?

- Everyone who lives or works in Switzerland (cross-border commuters)

- Swiss citizens abroad who work for the state or aid organisations

Obligation to pay AHV contributions

- Employed persons only: from 1 January of the year in which you turn 18 years old

- All: From 1 January of the year in which you turn 21. Until retirement age

- If you are still working at retirement age, you have an allowance of CHF 1,400 per month.

Interesting: The AHV is also financed by tobacco, alcohol, casinos, part of the VAT & part of the tax revenue.

How much is the AHV pension?

- Max. Withdrawal of AHV pension: 2 years (6.8% pension deduction per year withdrawn, lifelong)

- Max. Deferment of AHV pension: 5 years

- Contributions from age 18 – 20 can be taken into account (youth years)

- 5 years of additional payment possible

- Married couples receive max. 150% old-age pension (as of 2021: CHF 3’585.- per month)

Education and care credits are also credited when you register for retirement.

The education credits are credited automatically, while the care credits have to be claimed by you. In the 1st pillar, there is generally a debt to pay.

It is best to register at least 6 months before retirement, as this process can be lengthy.

The AHV is at its limit. It will be particularly tricky from 2030 onwards, as most baby boomers will retire then.

What happens to my AHV pension if I move abroad?

This depends on whether the country in question has an agreement with Switzerland.

- Country has agreement with Switzerland = Receives pension (only pension withdrawal possible, no lump sum)

- No agreement = no pension but must withdraw entire paid-in capital (without interest)

AHV survivors’ benefits

| 80% widow’s pension | – Min. 1 child (regardless of age) – Or 45 years and married for at least 5 years Pension until retirement unless she remarries |

| 80% widower’s pension | – Youngest child younger than 18 Pension only until youngest child is 18 |

| 40% orphan’s pension 60% orphan’s pension | – Up to the age of 18 or 25 (in education) |

Important: In the case of cohabitation, there is no survivor’s pension!

AHV Disability pension

- Integration has priority over pension

- 1 year waiting period before application

- Additional helplessness allowance of 120 – 912Fr, depending on the degree of severity.

- Birth defects: IV pays for medical treatment for up to 20 years. After that, the health insurance fund is responsible.

- IV children’s pension: Disabled persons with children: 40% child’s pension per child (child up to 18 or 25 years of age in education).

Supplementary benefits

Anyone who lives in Switzerland and receives an AHV pension or disability pension is entitled to supplementary benefits.

You must apply for supplementary benefits yourself.

There are two types of supplementary benefits:

- Money for insufficient income

- Sickness and disability-related expenses are paid for

Aid

The 1st pillar also covers the costs of certain aids.

These include:

| Hearing aids | Every 5 years |

| Wheelchairs without motor | Every 5 years |

| Wigs | Every year |

| Orthopedic shoes | Every 2 years |