So you want to file the tax return in Switzerland online, to save yourself the hassle.

Filing a tax return in Switzerland online is fast, but you know what’s even faster and simpler?

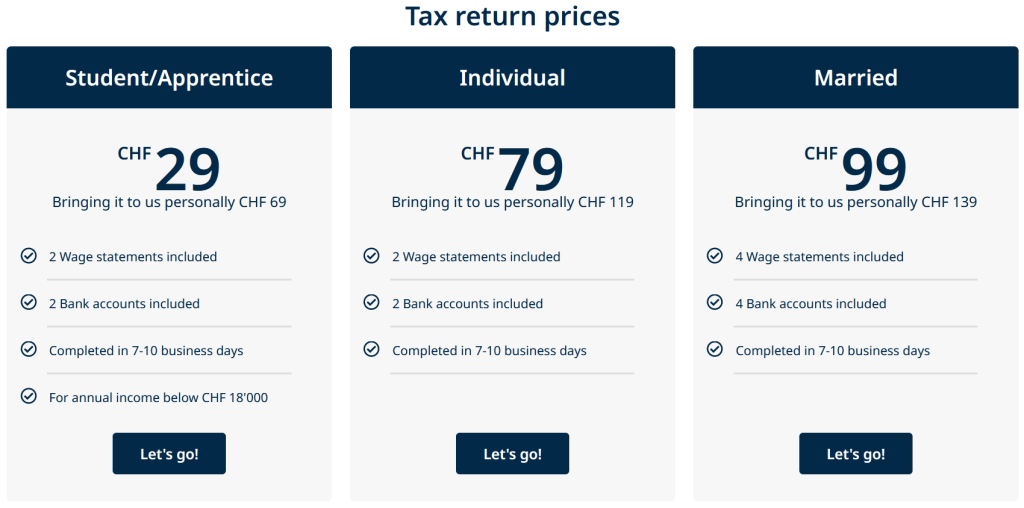

Having a team of tax experts fill out your tax return for you. This takes all work off your shoulders completely.

Over 2,000 customers throughout Switzerland trust the tax expertise of ajooda AG every year. Find out here why our customers are so satisfied and what they say about our service.

Taxation in Switzerland how does it even work?

You should keep the following in mind: Switzerland is a federal state, which means that there are 3 different levels of taxation: federal, cantonal and municipal.

Switzerland is known for its low taxes compared to other European countries and the rest of the world. However, the tax rate varies enormously and depends on where you live.

This means that for a married couple with a taxable income of CHF 100’000, the tax liability can range from CHF 7’530 to CHF 19’750, depending on where the couple resides.

What does it mean to be tax resident in Switzerland?

According to Swiss tax law, you are tax resident in the place where you have a permanent residence and which is the center of your personal and professional interests. In addition, anyone who stays in Switzerland for more than 90 days, or 30 days if you are working here, is also considered a tax resident.

In other words, if you hold a Swiss residence permit (L, B or C permit) and/or are registered as a resident with the local authorities, you are considered a tax resident by law.

However, international double taxation treaties may override this legislation.

When you file a tax return in Switzerland you must remember: As a Swiss tax resident, you are taxable with your worldwide income and assets (unlimited tax liability). While all taxable income and assets must be declared, certain income or assets are exempt from Swiss tax, such as income and assets from foreign real estate.

Those who are not considered tax residents in Switzerland due to domestic legislation or international tax treaties are only subject to Swiss tax on income or assets received in Switzerland (limited tax liability).

Withholding tax in Switzerland

Foreign employees, without a C permit, who work for Swiss employers are subject to Swiss withholding tax. The employer deducts this tax directly from the salary and delivers it to the tax authorities. Foreign citizens residents with a C Permit can file a tax return in Switzerland and declare their income and assets in the normal way.

The withholding tax is levied monthly by the Swiss employer and includes income tax at federal, cantonal and municipal level.

The income tax rate also takes into account the tax status, such as single, married or registered partnership, the employment status of the partner, dependent children, religious affiliation and certain flat-rate tax deductions.

The payroll tax deduction can be the final tax liability, unless one is entitled to claim pillar 3a deductions, alimony etc. in the tax return. Anyone wishing to make these pillar 3a deductions, for example, must apply for a subsequent ordinary assessment (NOV) until end of March of the year following the tax year.

Example: You want to do the tax return 2023, so you apply for the NOV until 31.03.2024 the latest.

Warning: Although its recommended to transit from withholding tax (Quellensteuer) to the tax return in 80-90% of cases, it is not certain that you will pay less tax with the tax return in the remaining 10-20% of cases, which could make a difference of a few thousand francs.

Easiest way to calculate the exact tax load is trough a professional tax adivsory like ajooda AG, to prevent any bad surprises.

Do I have to declare my income and assets in my tax return every year?

The payroll tax deduction by withholding tax is not the final tax liability and an annual income and wealth tax return must be submitted if one of the following circumstances applies:

- Acquisition of permanent residence status (C permit) or marriage to a Swiss citizen or C permit holder

- Annual gross salary of more than CHF 120’000 (CHF 500’000 for Geneva)

- Other substantial taxable income or assets that are not subject to Swiss payroll tax (i.e. investment income, real estate income, etc.)

Any payroll taxes withheld during the year will be credited against the final tax liability once the tax return has been audited by the tax authorities.

The deadline for filing the tax return is in most cantons the end of March of the year following the tax year and extensions are usually granted if requested in time.

The tax return must be filed with the cantonal or communal tax authorities of the respective place of residence.

File tax return in Switzerland – What must be considered?

In Switzerland the principle of family taxation applies. This means that income and assets of the spouse/registered partner and dependent children must be declared in a tax return. Separate filing is not possible.

One is obliged to declare worldwide income such as earned income, capital income, real estate income etc. in the tax return. Only a few elements of income are exempt from income tax, such as capital gains from movable property, casino winnings from gambling, etc., although exceptions are also possible.

In addition to the declarable income, certain deductions may be claimed. These deductions are usually divided into income-related, standard and social deductions. Depending on federal and cantonal regulations, different restrictions may apply.

Unlike many other countries, Switzerland levies a wealth tax on all assets at the end of each tax period (31st December). One is therefore obliged to declare all taxable assets such as bank accounts, investments, real estate, etc.

Some assets are tax-free, such as qualifying pension funds, household effects, etc. Since only the net assets are taxable, one is entitled to deduct all outstanding debts such as mortgages, loans, etc. from the taxable assets.

Ajooda’s tax tip when moving:

Taxes for the whole year must be paid in the municipality where you live on December 31st – exceptions are the cantons of Zurich, Nidwalden, Obwalden and Glarus, where the deadline is January 1st. Therefore it is wise to postpone the move to a more expensive place of residence until January.

On the other hand, it is highly recommended to move before January if the new place of residence is fiscally more favorable. This way you can live from January 1st to December 30th in an expensive place of residence and still be taxed at the low tax rate of the favorable canton, because you moved there on December 31st.

The only exceptions to this rule are the cantons of Fribourg and Neuchâtel, where taxes are divided between the communes, i.e. you pay taxes in both communes where you have lived for one year.